- What is Stablecoin?

- Main features of Stablecoins

- Types of Stablecoins

- Challenges and risks of Stablecoins

- How do Stablecoins work?

- What are Stablecoins used for?

- Difference from Traditional Cryptocurrencies

- Stablecoins as a part of the modern financial system

- How to buy Stablecoins?

- The practice of Cross-Border Stablecoins Payments

- Conclusion

According to Modern Monetary Theory, the central banks of various countries have a monopoly on the issue of money. After the abolition of the gold exchange standard, money became fiat money. That is, it is used by economic agents solely for this reason. The state legalizes it as a legal means of payment, circulation, and accumulation. Nevertheless, historical experience and studies of economists allow us to speak about the viability of the "free banking" system. There is no exclusive authority of the central bank to issue, and any institution gets the opportunity to give its own money. As a result of the competition of private capital through the market mechanism, the most suitable money is selected, which is ubiquitous. However, the state must legalize such money; otherwise it will not "work" or end up in a "grey zone" and be used in dubious transactions.

The creation of such a system in practice was hindered by the network effect, according to which the utility of using a good (in this case, money) depends on the number of users. In the conditions preceding the modern stage of development of information and communication technologies (ICT), the state had an incomparable advantage in terms of potential coverage of the population. However, digital money (digital money) can compete with public money by combining the properties of a universal medium of exchange and a payment system.

In today's blog, we want to consider such a phenomenon as a stablecoin, its disadvantages and advantages, and the types of how a stablecoin is used in the modern financial world.

In this article:

What is Stablecoin?

A stablecoin is a cryptocurrency whose rate is pegged to a real tangible asset, such as fiat currencies, securities, precious metals, real estate, natural resources, etc. The first stablecoin in 2015 was USDT (Tether), whose exchange rate was equal to the U.S. dollar. Since that time, several dozen varieties of stablecoins have appeared in circulation.

The primary purpose is to connect the world of cryptocurrencies with the material world. The need for such a bridge arose because there are no such concepts as the U.S. dollar, oil, or gold for the blockchain. For stablecoin, there is only a set of numbers and letters of the code, hash rate, number of transactions. The assets created based on the blockchain are tied to the universal transitional link's typical values.

Main Features of Stablecoins

The idea of creating a virtual currency became widespread in 2008–2009, which coincided with the acute phase of the global economic crisis, which weakened confidence in national and international financial institutions. Cryptocurrency developers have stated the need to create such payment systems based on cryptography and not trust, which would allow any two participants to transfer funds directly and without the participation of intermediaries.

In connection with the financial sector's digital transformation in 2014, unique digital assets appeared - stablecoins. This form has many advantages of virtual currencies (low cost of transactions, high speed of payments, anonymity, etc.), is based on the blockchain, and is devoid of the main drawback - high volatility.

Stability against fluctuations in the crypto exchange rate of stablecoins is achieved by linking stablecoins to various instruments, including fiat currencies, precious metals, digital cash, or by reproducing on a decentralized basis some elements of monetary policy used by central banks (the concept of Seigniorage Shares).

According to The Block Research, 110 million transactions worth more than $1 trillion were made using stablecoins in 2020. For comparison, the international payment system PayPal indicators are 15.4 billion transactions worth $936 billion (with the average transfer being about $60 for PayPal and more than $9,000 for stablecoins). This fact testifies to the significant potential of stablecoins for making transfers and payments. Now stablecoins are most often used for trading and large transactions. If it becomes clear to retail users that stablecoins are also suitable for microtransactions, their demand could skyrocket.

Benefits of stablecoins

- the impossibility of blocking funds due to the decentralized nature of transactions (through the blockchain);

- universality and lack of geographical restrictions when using;

- low exchange rate volatility due to stabilization mechanisms;

- low commission for payment transactions due to the absence of intermediaries represented by banks;

- high stability of peer-to-peer networks;

- high level of confidentiality;

- ease of use.

Opportunities

- ensuring a high level of anonymity;

- providing access to financial services without geographical or other restrictions;

- reducing the number of intermediaries in financial transactions;

- increase the speed of transactions;

- a new round of technological development that allows building an independent infrastructure from traditional banks and regulators;

- the possibility of building an innovative and decentralized financial system.

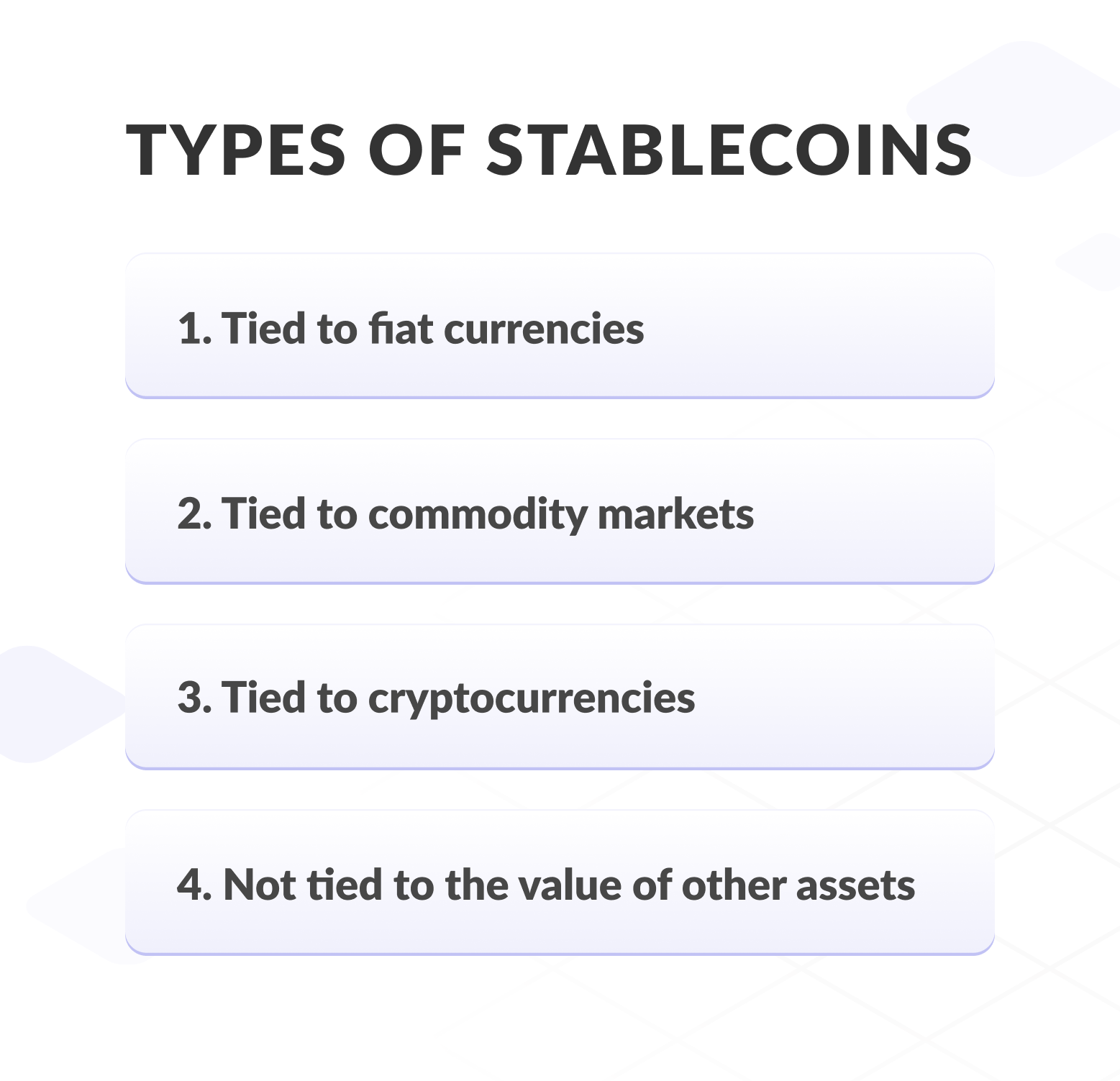

Types of Stablecoins

There are currently four types of stablecoins. We will discuss each type in more detail below.

1. Tied to fiat currencies

1. Tied to fiat currencies

This is the most common variety of stablecoins; their value is usually backed by the most popular currencies (U.S. dollar, euro, pound sterling, etc.). When converting such stablecoins, the organization that manages them exchanges fiat currencies for stablecoins. In this case, the equivalent amount of stablecoins is destroyed or withdrawn from circulation.

These stablecoins include:

- Tether (USDT), pegged to the U.S. dollar and holding 75% of the stablecoin market (as of January 1, 2021). It is the third largest cryptocurrency by market capitalization and has a higher daily trading volume than any other cryptocurrency, including Bitcoin.

- USD Coin (USDC) is also pegged to the U.S. dollar and is gradually increasing its market share (as of January 1, 2021, its share was 15% of the market). Visa is launching a project to issue corporate credit cards based on USD Coins.

- There are other stablecoins on the market backed by fiat currencies of the world: XSGD is pegged to the Singapore dollar, EURS is pegged to the euro, Candy is pegged to the Mongolian tugrik, etc.

2. Tied to commodity markets

The value of these cryptocurrencies is backed by fungible assets such as precious metals (such as gold), commodities (such as oil), or real estate. Often, such stablecoins are used for investment purposes.

Among them are:

- Digix Gold (DGX) is a gold-backed token operating on the Ethereum platform. One DGX corresponds to 1 gram of the precious metal. The gold collateral is held in Singapore, where the reserves are audited every three months. DGX holders can exchange cryptocurrency for bullion in Singapore.

- Tiberius Coin (TCX) is a stablecoin pegged to the value of a basket of seven precious metals used in the manufacture of high-tech equipment. It is assumed that with the spread of solar panels and electric cars, TCX will increase in price.

- SwissRealCoin (SRC) is a crypto asset backed by a portfolio of properties located in Switzerland. The holders of stablecoins determine the choice of such objects through voting.

3. Tied to cryptocurrencies

This type of stablecoin is backed by digital currencies, which leads to a high degree of decentralization since all operations are carried out through the blockchain.

In order to reduce the risks associated with high volatility, collateral is provided (most often in one of the fiat currencies). while the collateral value significantly exceeds the current value of the stablecoin.

There is an opinion that transactions in such stablecoins are safer and more transparent. To diversify risks, they can be tied to several cryptocurrencies. This type of cryptocurrency is not common. The most famous of these is Dai, backed by the dollar but backed by the Ethereum cryptocurrency.

4. Not tied to the value of other assets

This type of stablecoin has no collateral, and its turnover is based on the users' trust. The stability of the exchange rate of such a currency in the crypto world is determined by the issuer's intervention in the exchange rate formation process. With an increase in demand for a stablecoin, a currency is issued and distributed in the cryptocurrency market, which causes a decrease in its value. When demand falls, the issuer buys back the stablecoin, which causes its value to rise.

An example of such a currency is Ampleforth AMPL, launched at the end of 2018. The software algorithm underlying this stablecoin controls exchange rate dynamics and cryptocurrency's supply and demand volumes constantly. If necessary, it buys and sells it to stabilize the exchange rate.

Complete FinTech guide

Dive into all industry insights from our leading experts

Challenges and Risks of Stablecoins

Despite all the advantages, stablecoins have several risks that must be reckoned with.

Firstly, not all of them are more stable cryptocurrencies; despite the name — new projects appear but do not always survive. It is wise to use established stablecoins and gradually diversify into others.

Secondly, due to the linkage to other assets, they receive the following risks:

- The collapse of the price of fiat currency: even the euro and the dollar are getting cheaper, plus there are big failures.

- The collapse of the cryptocurrency currency (if tied to it).

- Legal restrictions: pegging to fiat currencies increases credibility and the number of requirements for enforcement. For example, Facebook launched its cryptocurrency based on different fiat currencies and got stuck in bureaucratic problems.

Thirdly, the owner of a stablecoin is one company with centralized management in most cases. Maintaining trust and stability requires constant monitoring, audits, and checks. Even the popular Tether, at some point, was rumored to offer a larger amount of cryptocurrency than real assets were. The U.S. Department of Justice has launched an investigation.

How Do Stablecoins Work?

The principle of using coins is similar to how we use physical money. In fact, the value of coins is almost always equal to assets in a ratio of 1:1, and the stablecoins themselves allow you to save capital carry out settlement or exchange. However, there are other options for currency reinforcement (which we discussed above).

Digital coins that are pegged to other cryptocurrencies may be dependent on one or more systems. Their stability is difficult to compare with how fiat-based digital coins are secured. But among the advantages of using such stablecoins is the ability to quickly and easily liquidate the currency, as well as decentralization.

Stablecoins without physical security are characterized by decentralization and are not limited to collateral obligations. Rate control is provided by issuers using smart contracts. For additional regulation, they resort to increasing or decreasing the issue of coins.

Stablecoins pegged to physical assets are equal in value to their fiat counterparts. If one coin is equal in value to a dollar, then physical money or assets are regarded as collateral for the value of the crypt. It is easier to protect such digital coins from hacker attacks, and besides, they are quite non-volatile. Among the minuses is the centralization of stablecoins.

What are Stablecoins Used for?

Like most digital assets, stablecoins are primarily used as a store of value and medium of exchange. They give traders temporary respite from volatility when the market drops and can also be used in the rapidly growing world of decentralized finance (DeFi) for things like yield farming, lending, and providing liquidity.

Most traders and investors gain access to stablecoins by buying them on exchange platforms, but it is also often possible to mint fresh stablecoins by depositing the necessary collateral with the issuing company, such as U.S. dollars or physical gold with CACHE gold.

Difference from Traditional Cryptocurrencies

Unlike the traditional crypto ecosystem, stablecoins are relatively stable. Since they are presumably backed by fiat currency, investors can be sure that their tokens will always sell for one dollar each. This supposedly means prices won't fall: coin prices are determined by faith, so if investors believe their stablecoins are worth and backed by one dollar each, the price should reflect that.

Stablecoins are a safe haven for worried investors. Many exchanges, including the world's largest Binance, do not allow traders to buy fiat currency but only allow them to buy and sell cryptocurrencies. This means that it is often difficult for investors to cash out their cryptocurrencies when the going gets tough quickly. To do this, they may have to make a transfer through several exchanges or even wait a few days.

This is where stablecoins come in. Because they are cryptocurrencies, they live on most exchanges. However, since they are pegged to the value of a single fiat currency, they act as a sort of temporary haven for investors looking to secure their funds during a bear market. In this way, stablecoins are like blockchain-enabled versions of the dollar. That is if they retain their value.

Stablecoins as part of the modern financial system

Economic agents prefer those monetary units that perform all the functions of money: measures of value, means of circulation, means of payment, and means of accumulation. Important is the fact of public recognition and legal support of the currency by the state. It can be assumed that the integration of global stablecoins into the world monetary system largely depends on their recognition by the international community.

It seems that the impact of stablecoins on the global monetary and financial system will be contradictory. According to the U.S. National Intelligence Council report, stablecoins and privately issued digital currencies pose a threat to central banks' implementation of monetary policy due to the emergence of parallel money circulation. In addition, regulators cannot fully control exchange rates and influence the money supply.

Now let's analyze the main advantages of stablecoins. Firstly, this digital currency can become an alternative to money transfers, reducing the time of transactions and commission. Secondly, stablecoins can be viewed as a "universal" means of payment, facilitating cross-border transfers in a single unit of account. In addition, stablecoins can remove other limitations of the existing payments ecosystem. In particular, their blockchain-based technology can help improve the wholesale clearing and settlement mechanism and simplify payment processes as well as multi-currency transactions while ensuring resilience to operational disruptions.

However, the massive use stablecoins comes with a number of risks. For example, stablecoins will not fully replace legal means of payment and act as a store of value. Often, the use of stablecoins leads to the realization of such risks as legal, financial, operational, as well as money laundering, and terrorist financing.

Therefore, stablecoins allow fast and low-cost payments, which requires effective financial, organizational, and technical conditions. However, in the absence of a proper regulatory system, various risks can arise, which can cause serious financial shocks.

How to Buy Stablecoins?

The purchase of a stablecoin is supported by many exchanges and exchangers. The most popular methods are the exchange through the Binance and Coinbase platforms. Binance recently added support for fiat currencies, allowing you to buy cryptocurrencies directly from your card using partners that process fiat payments. Cryptocurrency enters the exchange balance.

Coinbase is a safer way to buy USDT with USD. In addition, the site allows you to store cryptocurrency on a personal account safely and is available to U.S. citizens.

The practice of Cross-Border Stablecoins Payments

In 2019, Facebook initiated the development and implementation of the Libra project in order to create a digital currency that users of the social network (more than 2.7 billion people) can use. The developers announced the binding of this stablecoin to four fiat currencies. The U.S. financial authorities expressed extreme concern about this initiative, as they saw in its implementation a threat to the stability of the modern (dollar) financial system.

In March 2021, Visa became the first international card payment system to conduct transactions using the USD Coin (USDC) stablecoin through the Crypto.com blockchain platform. Mass transactions using stablecoins will become available by the end of 2021. According to Jack Forestell, executive vice president, head of products at Visa, ''the use of stablecoins is the next step towards securing payments in various currencies around the world.''

At the beginning of 2021, Mastercard announced the start of work with stablecoins: customers will be able to use them for investments and transactions.

Obviously, international payment systems are striving to maintain a dominant position in the payment services market, using their advantages in the form of brand recognition, user trust, and an established infrastructure to compete with alternative financial platforms that are gaining popularity.

Conclusion

Against the backdrop of the volatility of cryptocurrencies, ''stable coins'' are actively gaining popularity, combining the advantages of both decentralized currencies and fiat money. This trend is also reflected in the policy of the world's leading payment systems, which, in order to maintain their positions in the competitive market, integrate stablecoins into their payment networks. It demonstrates the urgent need for innovative financial institutions' creative development and improved technologies and business processes in FinTech software development services.

The emergence and development of stablecoins are becoming a clear trend in the financial sector, which determines both the realization of risks and potential opportunities. The issuance of stablecoins by commercial banks (JPMorgan, etc.), as well as the development by many countries of state digital currencies and the creation of a global stablecoin by the international community (the Financial Stability Board, the International Monetary Fund, the Bank for International Settlements, the FATF, etc.), suggest a significant potential for application this innovative tool. The high interest of investors in this asset and the growth in the capitalization of stablecoins confirm this. We should not forget about the risks of this digital tool, primarily the regulatory risk.

In the long term, due to the active development of innovative technologies in the financial sector, we can expect a serious transformation of the global financial system, both due to changes in its infrastructure components (settlement and payment systems, information exchange and transfer mechanisms, etc.) and in connection with decentralization financial relations.